The Arizona Department of Administration provides medical insurance to state employees, including University of Arizona employees and their legal dependents. Review the information below carefully for details on your options.

Steps and Considerations When Choosing a Medical Plan

Note: You may only choose a medical plan during new hire benefits enrollment, the annual fall benefits open enrollment period or if you experience a qualified life event.

Step 1: Compare Medical Plan Options

Quick downloads: Definitions & Quick Facts

2026: 2026 Plan comparison chart | 2026 medical premiums | 2026 Benefits Guide (PDF) | 2026 Benefits Summary (PDF) | 2026 Insurance Premiums for Employees Paid over Nine Months (Coming soon)

{kind=link}

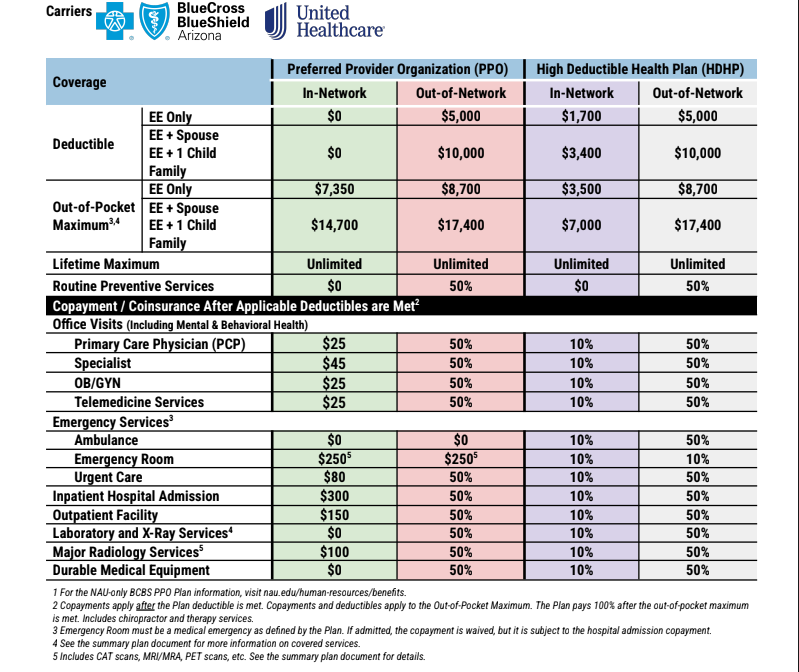

Preferred Provider Organization (PPO) Plan

The PPO has higher monthly premiums but no deductibles for in-network care.

You pay copays for most services (primary care $25, specialist $45, emergency room $250). Once you reach the out-of-pocket maximum in the plan year ($7,350 employee / $14,700 family), you pay nothing.

$0 copay for preventive care. Prescription copays range from $15-$60 and are not subject to the deductible.

Compare Plans: Blue Cross Blue Shield and UnitedHealthcare networks

Plan Documents - PPO

NEW 2026 PPO Summary of Benefits and Coverage - English (PDF)

NEW 2026 PPO Summary of Benefits and Coverage - Español (PDF)

2026 PPO Summary Plan Description (PDF) (Coming Soon)

NEW Glossary of Health Coverage and Medical Terms (PDF)

High-Deductible Health Plan (HDHP) with Health Savings Account (HSA)

The HDHP has lower premiums and is paired with an HSA.

You are responsible for the cost of services until you meet the deductible. Once you meet the deductible, you pay 10% (coinsurance), and the plan pays 90% until you reach the out-of-pocket maximum. Once you reach the out-of-pocket maximum, you pay nothing.

With the HDHP, the university will open an account on your behalf with Inpsira and contribute to your HSA every pay period ($30 for employees and $60 for family). You may also choose to contribute for additional tax savings.

Your HSA monies can be used toward your deductible, coinsurance, or other qualified medical expenses. All preventive services are free and do not count toward the deductible. You do, however, pay a copay for preventive prescriptions.

Compare Plans: Blue Cross Blue Shield and UnitedHealthcare networks

Plan Documents - HDHP With HSA

NEW 2026 HDHP Summary of Benefits and Coverage - English (PDF)

NEW 2026 HDHP Summary of Benefits and Coverage - Español (PDF)

2026 HDHP Summary Plan Description (PDF) (Coming Soon)

NEW Glossary of Health Coverage and Medical Terms (PDF)

You are ineligible for the HDHP if you have a Health Reimbursement Account or coverage through Medicare or TRICARE. You also cannot be claimed as a dependent on another person’s tax return.

Step 2: Compare Insurance Carriers

The provider networks may differ between the two insurance carriers. Search for your providers with both carriers to help determine your best choice.

Blue Cross Blue Shield of Arizona

Find network doctors and facilities

- Visit www.azblue.com/stateofaz

- Scroll down and click “Find a Doctor.”

- Choose a network: PPO OR High Deductible Health Plan. Click “Find a Doctor.”

- Be sure to update your location and network settings in the upper-right corner. The network should be set to “Statewide/National PPO/EPO with Mayo.”

- Search by name or specialty.

UnitedHealthcare

Find network doctors and facilities

- Visit www.whyuhc.com/stateofaz

- Click on the “Providers” tab.

- Select the applicable medical plan

- Enter your search location

Preferred Provider Organization (PPO) Plan

- This plan has higher premiums but no deductible for in-network care.

- You pay predictable copays for services: $25 for primary care, $45 for a specialist, $250 emergency room, $300 hospital admission.

- Once you reach the out-of-pocket maximum ($7,350 single / $14,700 family), you pay nothing.

- No tiers to navigate - one simple structure for all in-network providers, making it easier to understand your coverage.

- Because you pay fixed copays rather than meeting a deductible first, you'll have predictable costs from your first visit.

- Preventive care is $0, and prescription copays ($15-$60) are not subject to a deductible.

- This plan may work well if you prefer budget predictability and visit doctors regularly.

High-Deductible Health Plan (HDHP) With Health Savings Account (HSA)

This plan has higher deductibles of $1,700 (single) or $3,400 (family) but much lower premiums.

- If you are generally healthy and receive mostly preventive and routine care, your out-of-pocket costs may be less.

- If you have unexpected medical expenses, you may experience higher out-of-pocket costs because of the deductible and the less predictable 10% coinsurance.

- The university contributes to an HSA account each pay period to help you cover the deductible, coinsurance, or other qualified medical expenses. Annually, this contribution is $720 (single) or $1,440 (family) - about half of the deductible.

- You may make pre-tax contributions to the HSA through payroll deduction, allowing you to build tax-free savings to pay for healthcare. You also do not pay taxes when you withdraw the money to pay for your medical expenses.

- All funds in the HSA belong to you. There is no use-it-or-lose-it requirement, and you can keep your HSA even if you leave the university.